Most reference interest rate LIBOR have already been replaced at the end of 2021. As of the end of June 2023, the publication of the latest LIBOR reference rates in USD will now also be discontinued. A project team is dealing with the effects of the conversion of processes, systems and products within LGT and is implementing the necessary measures. On this page you will find all relevant information about the LIBOR transition. The page is updated regularly.

FAQ

1. What is LIBOR?

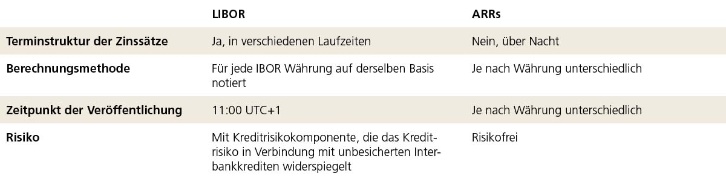

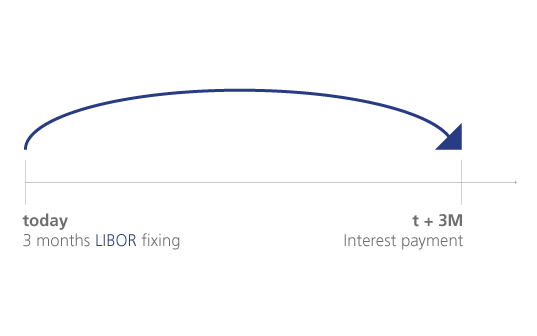

Interbank Offered Rates (IBORs), which include LIBOR (London Interbank Offered Rate), are reference interest rates that have been published since 1986 and are used to calculate the cost of short-term, unsecured loans. A defined group of banks (the so-called contributor panel banks) provide daily estimates of their interest rates for a number of currencies and tenors, the average value of which is calculated and published. They are used as reference rates for financial products. These include mortgages, other loans, floating rate notes, structured products and derivatives. They often also serve as a basis for valuations or calculations, for example for performance-based fees for investment funds. The interest amount that can be expected at the end of the contract period for longer-term IBOR based contracts are already known on the day the transaction is concluded – this is one of the significant differences to the new reference rates. Further information can be found under point 5.

2. Why is LIBOR being replaced?

In 2011, manipulations of the reference rates LIBOR, Euro Interbank Offered Rate (EURIBOR) and Tokyo Interbank Offered Rate (TIBOR) were uncovered. LIBOR is based on the market estimates of a few banks and can therefore deviate slightly from market conditions. A review of the main reference rates conducted in 2013 showed that even after reforms to strengthen the methodology, certain risks relating to the stability and reliability of IBORs could not be completely ruled out. The UK Financial Conduct Authority (FCA) therefore decided in 2017 to no longer require the panel banks to provide LIBOR reports from the end of 2021. The announcement by the UK Financial Conduct Authority triggered the process to replace the IBOR reference rates.

The new reference rates are coordinated by the Financial Stability Board (FSB) on behalf of the G20 countries. In addition to central banks and supervisory authorities, an international group of financial market participants from the banking sector is also involved. The latter is examining alternative reference rates that better meet the needs of the market and the requirements of the supervisory authorities in the longer term. The focus here is on improving the transparency, methodology and supervision of reference rates in order to ultimately restore the representativity and confidence of market participants.

3. What are the alternatives to IBORs?

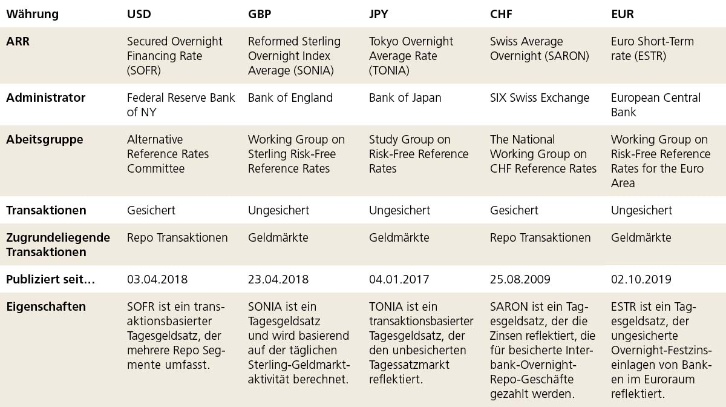

Instead of IBORs, so-called alternative reference rates (ARRs) will be applied. Working groups from various nations and currency have defined and established these new reference rates, whose calculation mechanism varies from currency to currency.

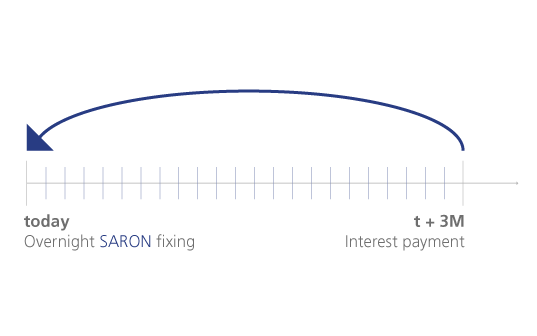

In contrast to the IBORs, the ARRs are no longer based on estimates, but are linked to active and actually traded call money rates and are therefore considered robust, transparent and almost impossible to manipulate. What all the new rates have in common is that the effective interest amount is only known at the end of an interest calculating period if it is longer than one day. This results in the need for extensive adjustments, which the LGT project team will implement for the client.

Here you find an overview of various ARRs:

The Swiss National Bank and the stock exchange operator SIX already issue and use SARON (Swiss Average Rate Overnight). The average interest rate is calculated based on priced transactions in the order book of the SIX Repo platform. The determination of the interest rate is subject to constant monitoring. In the euro zone, ESTR (Euro Short Term Rate) has replaced the previous EONIA (Euro OverNight Index Average). According to the European Securities and Markets Authority (ESMA), the reformed EURIBOR of the administrator European Money Markets Institute (EMMI) is compliant and will therefore remain in place.

In the US, the USD LIBOR will be replaced by the Secured Overnight Financing Rate (SOFR). The SOFR is an interest rate that is paid for overnight borrowing secured by US government bonds. It is calculated and published daily by the Federal Reserve in New York in cooperation with the Office of Financial Research.

For contracts with a term of one week to two months, the transition from USD LIBOR to SOFR has taken place at the end of 2021, at the same time as other currencies. For USD LIBOR contracts where LIBOR is applied with a maturity of one month and three months or more, the conversion will take place no later than June 2023. Please note that LGT is not allowed to conclude new contracts on a USD LIBOR basis due to the changeover. We offer interested clients investment opportunities in the new ARRs. If you have any questions, please do not hesitate to contact your LGT contact person. For clients, the new ARR interest rates offer advantages because – unlike IBORs – they are based on market transactions and are monitored accordingly.

4. When will the new ARRs start to apply?

The new ARRs have already been established on the market for some time. The regulators have stipulated that LIBOR based contracts should no longer be launched.

5. How are the ARRs calculated?

Although ARRs will functionally replace LIBOR as a benchmark in global financial markets, it is important to understand that they are calculated in fundamentally different ways.

In contrast to the IBORs, the ARRs are no longer based on estimates, but are linked to active and actually traded call money rates and are therefore considered robust, transparent and almost impossible to manipulate.

The new ARR based contracts are calculated daily based on these ARRs – meaning that the exact interest rate is available at the end of the contract’s term. As a result, the final valuations at the end of the contract term are always only available retrospectively – this is a key difference to the previous IBOR method.

In summary, the following should be noted:

In most currencies, the changeover of LIBOR was successfully completed by the end of 2021.

The current conversion affects only a few maturities in USD.

Existing IBOR-based contracts are to be converted in time or replaced by new ARR-based contracts.

In contrast to IBOR contracts, ARRs are valued by a transparent, daily calculation.

Here is a summary of the main differences between IBOR and ARRs:

The new ARRs do not include credit and liquidity premiums. The new ARRs are overnight rates, and depending on the market, ARRs are collateralized or uncollateralized. The new ARRs involve the use of daily fixed rates (compounding overnight in arrears), which means that the final interest amount of the contract will not be known until the end of the interest period. Forward-looking interest rates for ARRs could still become available in case of specific needs - such as the valuation of the contracts at the end of the year - but the timing of the provision of such ARRs is still to be defined by the regulator.