Private individuals were prohibited from owning gold in the US for decades. This was followed by a wild bull market for precious metals with a sudden end.

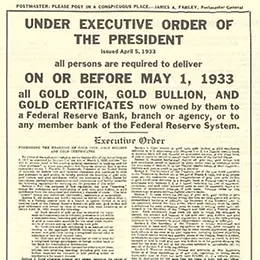

Historical announcement that the private ownership of gold is prohibited in the US.

Gold has been known and coveted almost everywhere in the world for thousands of years. In addition to its function as a means of payment - in the form of coins - it was used to back assets long term.

Today, gold is an asset class in its own right and differs from other metals used in manufacturing such as silver, platinum and palladium. But investors have not always been able to invest in it. Records show that in ancient Sparta, private ownership of precious metals was punishable by death. The private ownership of gold was also prohibited in a number of countries later in history, such as in the US from 1933 to 1974.

Some background: Gold under Bretton Woods

Awareness of the value of gold has increased over time. This combined with its limited availability means that gold was also used to back currencies - especially under the new Bretton Woods monetary system introduced after World War II.

At that time, the US possessed about two-thirds of the world’s gold reserves. With the aim of bringing stability to the world’s currencies and stimulating international trade, the US dollar was thus pegged to it.

Over the years, the system’s member countries accumulated such vast reserves in US dollars due to their current account surpluses that they exceeded the US's gold holdings. The agreed conversion rate of 35 US dollars per troy ounce of gold thus became practically non-executable and confidence in the US dollar was lost.

In 1971, the US finally unpegged the dollar from gold (the "Nixon Shock") and in 1973, the Bretton Woods system came to an end. Most currencies became free floating. Since then, gold has played an insignificant role in international payment transactions.

The drivers of the commodities boom

In addition to the instability of the Bretton Woods system, another problem emerged in the global economy: inflation rates began to rise at the end of the 1960s. One reason for this was that the US wanted to improve the employment situation through expansionary monetary policy. In addition, national debt had risen significantly as a result of the Vietnam War. As a result, the US dollar became increasingly weaker during the 1970s. According to Macrotrends, it depreciated by around 20 percent between 1973 and 1979. This drove up the price of gold and commodities in general.

Two of many reasons for turning away from the Bretton Woods system: Vietnam War and mass unemployment.

This trend was additionally fueled by geopolitical crises. Gold reached its record high in January 1980, two months before the start of the hostage-taking at the US embassy in Iran. Less than a month earlier, the Soviet Union had invaded Afghanistan.

The rising gold price was therefore likely a result of panic buying in the US. As in later crises, buyers saw gold as a (supposedly) safe haven. However, the markets were not as developed and liquid as they are today. Many people were betting on the same idea, and the price movements were accordingly extreme. After having been banned for decades, private investors in the US may also have lacked the expertise in dealing with the "new" asset class.

Machlup was wrong

In his 1969 paper "Speculations on Gold Speculation", the well-known economist Fritz Machlup concluded that the gold price of 35 US dollars per troy ounce that applied under Bretton Woods, would decline significantly if demand from governments ceased to exist.

He believed that the idea that gold has a permanent intrinsic value was a myth purported by the central banks. But further developments showed the opposite: after many years of prohibition and being pegged to the dollar, gold remained attractive in people's minds - as a means of payment and preserving assets, and increasingly as an investment as well as for speculation.

The long lasting trend in gold ended at a time when the inflation rate in the US reached double-digit levels. The Fed Chairman at the time, Paul Volcker, pulled the emergency brake. He briefly raised interest rates to around 20 percent. In doing so, he managed to stifle inflation, which was a key driver of the gold boom, between 1980 and 1981.

The wild 1970s and the subsequent declines in the gold price has become etched in the memory of many investors. Only after a 20-year bear market did interest in precious metals slowly return. In contrast to back then, gold today tends to be used for portfolio diversification purposes. Excesses like those at the end of the 1970s have not been seen since.

Long-term investment trends - could they be an opportunity for you?

Long-term investment trends play an important role in LGT's investment advisory services. If you are also interested in current global market and economic developments, we recommend that you read some of the insights provided by our research experts.

Related

Financial markets

Nifty Fifty: A boom in growth stocks

As with many investment trends, historical developments facilitated the emergence of the boom of the so-called Nifty Fifty. Due to the Vietnam War, national debt in the US during the mid- to late 1960s was a cause of great concern among investors. Many feared inflation, and therefore focused...