Back in December 2021, we analyzed the causes of the significant surge in inflation and its impact on the equity markets in light of current events. In the following, we shed light on how the situation has evolved over the course of 2022 and which scenario could come to fruition in the short and medium term. In this context, three developments in the first half of 2022 stand out massively.

1. The Russia-Ukraine conflict

The invasion of Ukraine by Russian troops on February 24, 2022, has contributed significantly to an additional supply-side inflation shock. Russia is a major supplier of raw materials of all kinds, including energy sources such as oil, natural gas and coal, metals such as palladium, platinum, nickel, steel, aluminum and copper, and foodstuffs such as grains (e.g. wheat) as well as fertilizers, which are essential for food production.

As a result of its belligerent activities, Russia very quickly became the world's most sanctioned country, leaving countries such as Iran far behind in this respect. This exacerbated supply shortages and what were already significant disruptions in supply chains, which in turn manifested itself in increased supply and inflation shocks for selected commodities. The European Union, as one of Russia's largest trading partners, was disproportionately affected. The greatest risk for the EU, however, is a complete halt in the supply of Russian natural gas.

Before the war, Russia covered about one third of Europe's natural gas needs, which has since become much less. This makes it difficult to build up natural gas stocks before the coming winter and leads to significantly higher natural gas and energy costs on the European continent compared with the USA. Ultimately, this leads to competitive disadvantages for Europe and keeps inflationary pressure correspondingly high.

2. Renewed lockdowns in China

With the burgeoning of the omicron variant, China experienced its strongest corona outbreak since the spring of 2020. As of mid-March, some 375 million people in 45 cities were temporarily in renewed "lockdowns."

Affected areas included large parts of the Yangtze River Delta, which, with its major cities, technology and manufacturing hubs such as Shanghai, Zhejiang and Jiangsu, accounts for only 11.4% of the population but is responsible for around 21% of industrial production and 36% of China's exports. At times, long queues of up to 500 container ships formed at Shanghai's port facilities - the world's largest cargo handling hub - unable to dock, unload or reload.

At the height of the traffic chaos, about one-fifth of the global container fleet was stuck unproductively on various coasts. By land, China's new Silk Road, more than 6,000 kilometers long, runs through Ukraine to Moscow and on to Europe. As a result of the war in Ukraine, containers could not be transported via this route as scheduled, further shifting the transport load to ships and contributing to supply chain disruptions.

Finally, daily domestic flights in China had fallen from over 14 000 at the beginning of the year to less than 3 500, similar to the start of the Corona pandemic in spring 2020. A slowdown in the world's second largest economy had a corresponding impact on the global economic momentum. Although the situation has improved in the meantime, experts believe that China is likely to stick to the "zero-covid" policy at least until the 20th Party Congress of the Communist Party Congress in the fall, which entails the risk of renewed or continued disruptions. In the Chinese home market, the recent lockdowns accelerated a gradual exodus of important supplier industries.

3. Clear change of course by central banks

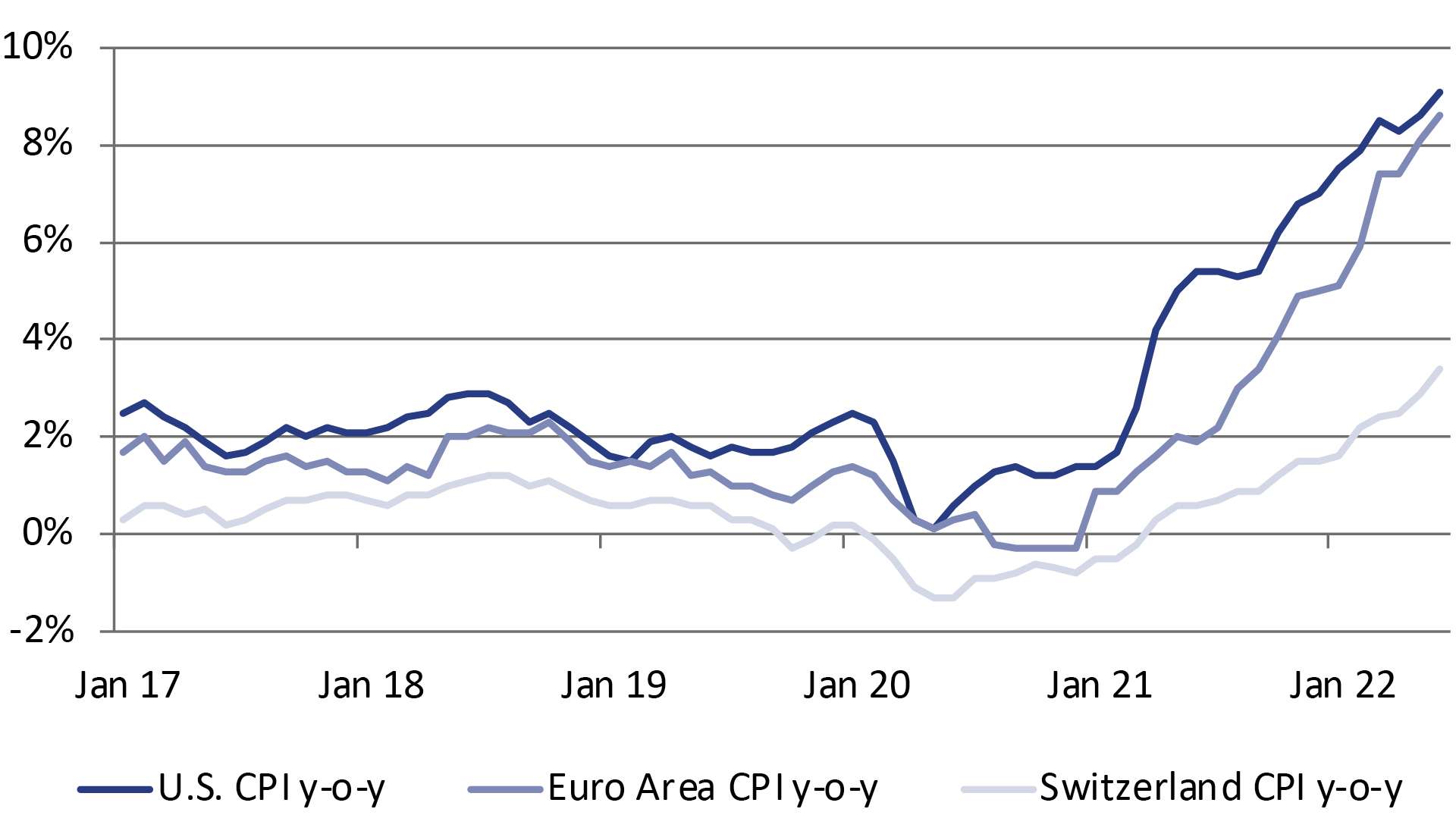

Chart 1: Inflation trend in the month of June. Source: Bloomberg.

Accordingly, inflationary pressures remained higher and longer than originally anticipated, mainly as a result of supply-side problems. The latest inflation figures for the month of June reached 9.1% year-on-year in the U.S., 8.6% in Europe - both highs in around 40 years - and even in Switzerland a remarkable 3.4% - the highest level in 14 years (Chart 1).

The strong Swiss franc is helping to keep inflationary pressures on imported goods - including oil and natural gas - somewhat in check. In response to the persistently high inflationary pressures, the U.S. Fed already started tightening the monetary policy screws in the first half of the year. Key interest rates were raised several times, once by as much as 75 basis points.

The last time interest rates were raised so sharply was in 1994, some 28 years ago. Even the Swiss National Bank (SNB) dared to raise interest rates by 50 basis points, thus reacting faster than the European Central Bank (ECB). This has contributed to a clear strength of the U.S. dollar as well as the Swiss franc against the euro.

However, the ECB is expected to follow suit with rate hikes as well. Thus, the focus of central banks has clearly shifted from stimulating the economy to fighting inflation. The tightening of liquidity conditions is also causing problems for market participants.

Impact

The massive trade sanctions and embargoes against Russia have caused many Western companies to exit the Russian market. Three decades of foreign investment have collapsed almost overnight, and various Western companies have suffered large write-downs on their holdings and assets. The damage from this is almost irreparable and is setting Russia back massively economically.

China is seeking a path of relaxation in dealing with zero tolerance with Covid-19, but this is proving difficult. The Chinese government's policies toward its people have positioned it as clearly superior to the West. The party’s political leadership has paraded the capitalist West before its people as merciless, millions of lives would be risked or even sacrificed to maintain consumption and capitalism. An elegant way out of the current Corona strategy without losing face is therefore difficult.

The Chinese government is countering the difficulties in its home market with an easing of monetary policy and increasing stimulus measures. This makes China one of the few economies that is enjoying a growth recovery from an already low level supported by monetary and fiscal tailwinds, while the rest of the world is actually going in exactly the opposite direction - towards a slowdown in economic momentum accompanied by lower liquidity to get inflation under control.

However, ongoing regulatory pressure, an overvalued real estate market and the problematic zero-tolerance policy pose above-average risks. With regard to global supply bottlenecks - clearly excluding isolated commodities such as natural gas or food - moderate improvements can be witnessed. The situation is beginning to ease. Container ship congestion is declining, the availability of truck drivers has improved, freight rates are falling and delivery times are shortening. However, this is not only due to advances in logistics, but predominantly to declining demand.

In many areas of the economy, as a result of delivery problems, too much has been ordered in stock, demand has been overestimated, and inventory is growing, which in turn leads to cancellations of pending orders. This phenomenon is called "demand destruction." When supply is tight, weakening demand reduces upward pressure on prices, i.e., as a result of lower demand, the imbalance between supply and demand is reduced, which should ease inflationary pressures over time.

Overall, however, difficult conditions have given equity markets one of their worst first half-years in decades. The U.S. stock market, for example, had its worst first-half performance since 1962 - that is, in 60 years.

Consumers have to tighten their belts

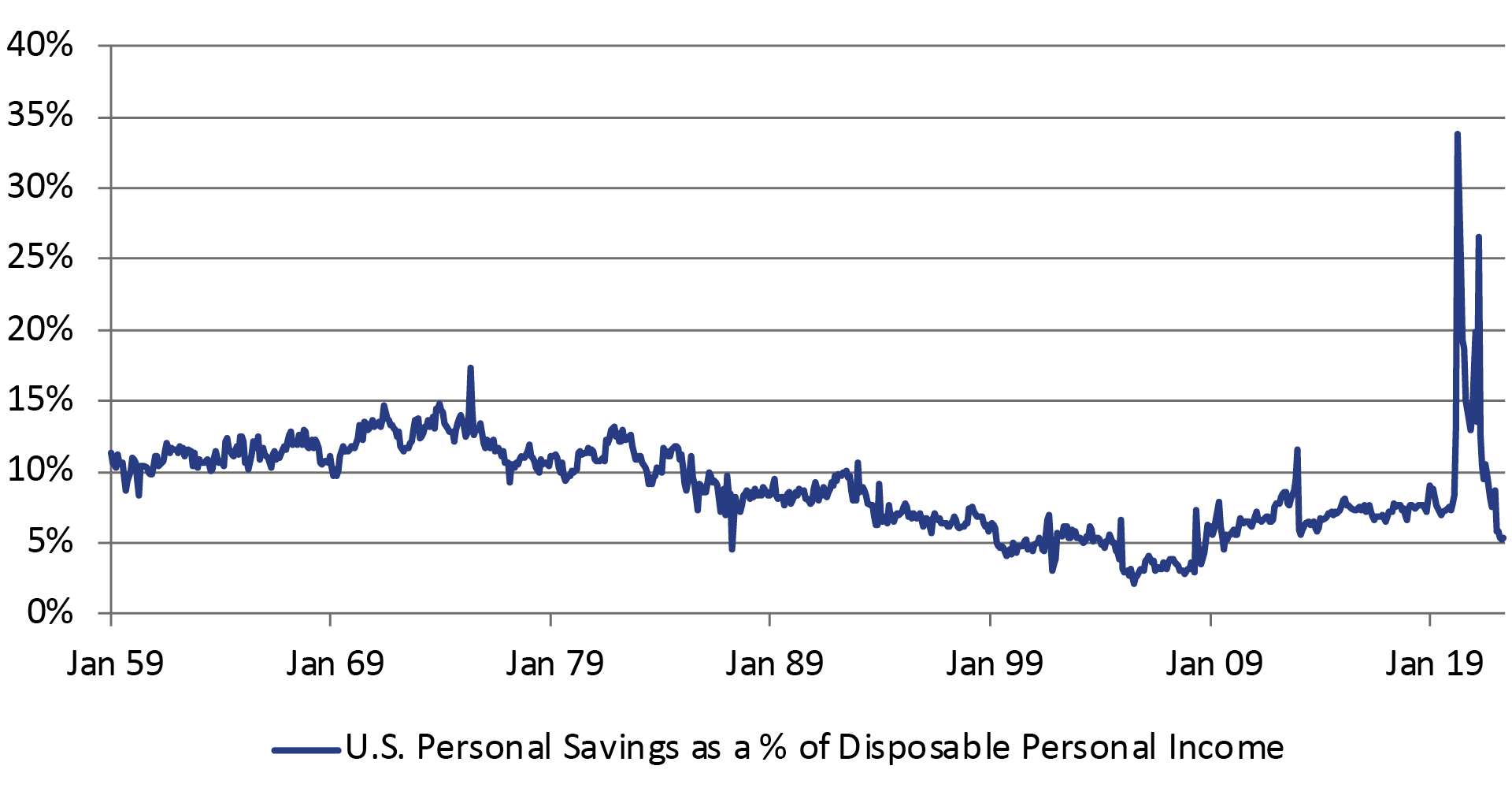

Chart 2: U.S. savings rate as % of disposable income. Source: Bloomberg.

Wage growth has so far been unable to keep pace with persistently high inflation - especially in vital areas such as food, energy or mortgage refinancing costs - which is why consumers are experiencing a real reduction in purchasing power. In other words, they can no longer afford as much as they used to.

In consumer surveys in the U.S., nearly 50% of respondents say they are having to curtail their spending patterns, especially in less essential non-basic consumption. The term "fuel poverty" was born. It refers to consumers who are struggling financially to cover even the essentials of life. Some consumers have to decide whether to use their budget for fuel, heating or food.

In some countries, such as Germany or the United Kingdom, almost 20% of households seem to fall into this category. This now also explains the phenomenon of demand destruction described above. The combination of inflation, a drop in real wages and higher financing costs leads to lower demand for consumer goods and services. Those who continue to consume blithely do so partly by taking on more debt, be it credit card debt or personal loans.

Chart 2 shows impressively that the savings rate of U.S. consumers - albeit from an enormously high savings buffer that they were able to build up thanks to generous assistance during the Corona pandemic - has now fallen to its lowest level since 2009. On the one hand, such consumption behavior shows that consumers can absorb the inflation shock to a certain extent via their savings in the short term, but on the other hand, consumption by depleting savings or increasing credit loans can only be sustained to a limited extent in the longer term.

What’s next?

Chart 3: Broad commodity indices started to correct. Source: Bloomberg.

The peak of U.S. inflation has been predicted for some time, and repeatedly postponed. However, there are now increasing signs that inflationary pressure in the U.S.A. is likely to ease in the third quarter. Declining demand - possibly also a mild recession - coupled with better-oiled supply chains should contribute to this. In Europe, the situation is more difficult.

A latent energy crisis hangs over Europe. The European market is more dependent than average on gas supplies from Russia, above all Germany, Italy and Austria. As Germany continues to export Russian natural gas, this is becoming a Europe-wide issue. As early as June, Russia began to cut natural gas supplies via the most important pipeline, Nord Stream 1, and ultimately delivered just under a third of the contractually agreed volume. On July 11, Nordstream 1 was shut down for ten days to carry out annual inspection work.

Concerns are high that Russia could leave the gas tap shut after the overhaul. Our scenario is that Russia may first delay a resumption of gas supplies a bit, playing for time for a few days or a week to keep nervousness high in Europe. After that, however, Russia is likely to release up to an estimated 40% of the agreed supply volume. If Nord Stream 1 were not used at all for an extended period, there would be extensive damage that would be difficult to repair.

By delivering up to 40%, Russia achieves two important goals: First, a sustained high natural gas price, and second, Europe cannot increase its stockpile to the desired 80% before winter (currently about 50%), which anticipatively strengthens Russia's negotiation power. The inflation scenario for Europe is therefore more difficult to assess. We expect inflationary pressures to peak in Q4 2022 or Q1 2023 at the latest. A key reason is the slowdown in global demand described above, which is also reflected in an initial, moderate decline in commodity prices (chart 3). The ongoing cooling of economic momentum also points to an increased risk of recession. However, in both key regions - the USA and Europe - inflation is likely to remain at visibly higher levels for the time being than before Corona, for example, even after it has passed its peak.

The correction on the stock markets in the course of the year to date already to a certain extent prices in the difficult environment with slowing economic growth, increased risks of recession as well as continuing inflationary pressure and a lower supply of liquidity to the markets by the central banks. What is still missing are downward revisions to earnings expectations.

In our view, earnings expectations are holding at too high a level in view of the significant rise in manufacturing costs. Weaker economic momentum, more modest earnings expectations - also a sign of weakening demand - and thus easing inflationary pressures would give central banks the opportunity to move away from a tight monetary policy stance, thus giving equity markets more room to breathe again. Until then, continued increased volatility on the stock markets is to be expected.

Impact on the equity strategy

Due to the higher degree of energy self-sufficiency, the corresponding competitive advantages in terms of cheaper production and the better visibility regarding the development of inflation, we prefer the U.S. stock market to the European one. In Europe, companies pay more than four times as much for natural gas and the price of electricity has multiplied compared to the pre-Corona pandemic period.

We are pursuing a scenario in which Europe can count on a minimum supply of natural gas from Russia, but the risk of an escalation in energy supply hangs like a sword of Damocles over the European stock market for the time being. Europe's advantages due to a weak euro - which supports exports but makes commodity imports more expensive - cheaper valuations, solid balance sheets and the fact that global investors already seem to be significantly underweighted in European equities do not fully outweigh the short-term risks. We therefore prefer the U.S. equity market ("attractive") to the European one ("unattractive").

Market information from our research experts

How we see the markets

LGT’s experts are always busy analysing global economic and market trends. Our research publications on the international financial markets, sectors and companies will help you make informed investment decisions.