在此处更改您的语言和 LGT 位置。

私人客户的数字平台

登入 LGT 智能银行

金融中介机构的数字平台

登入 LGT 智能银行 Pro

常见问题解答 (FAQ)

LGT 智能银行帮助

常见问题解答 (FAQ)

LGT 智能银行专业版帮助

Demographic trends vary significantly in different countries and regions. What does that mean for investors?

Naturalist Sir David Attenborough has highlighted the damaging impact a growing human population has on the planet. The pressure on resources will only increase in the years to come. However, the picture is far from uniform and, in many parts of the world, the population is declining.

While controlling the birth rate may slow population growth, advances in medicine and better living conditions mean that life expectancy is rising. The burden of an aging population will also be felt, as in some countries the number of people of working age declines, meanwhile those beyond retirement age rises. This may have profound implications for investors in the long run, but in the short term it may be harder to observe the impact. In an effort to take a longer-term view, we will look at these trends to see what can be inferred for investors.

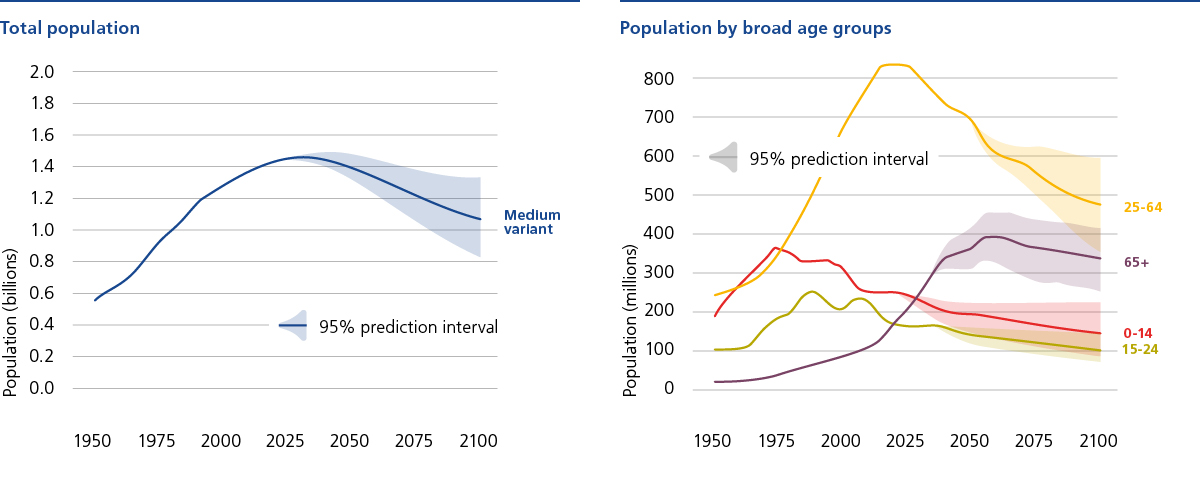

The charts in this report, taken from a United Nation study on population trends, clearly show that different countries and regional profiles vary considerably. Demographic changes are slow to develop and changing the trend is very difficult. The ecological and financial consequences may be substantial. Anyone making long-term financial plans should consider these trends as the look at their future.

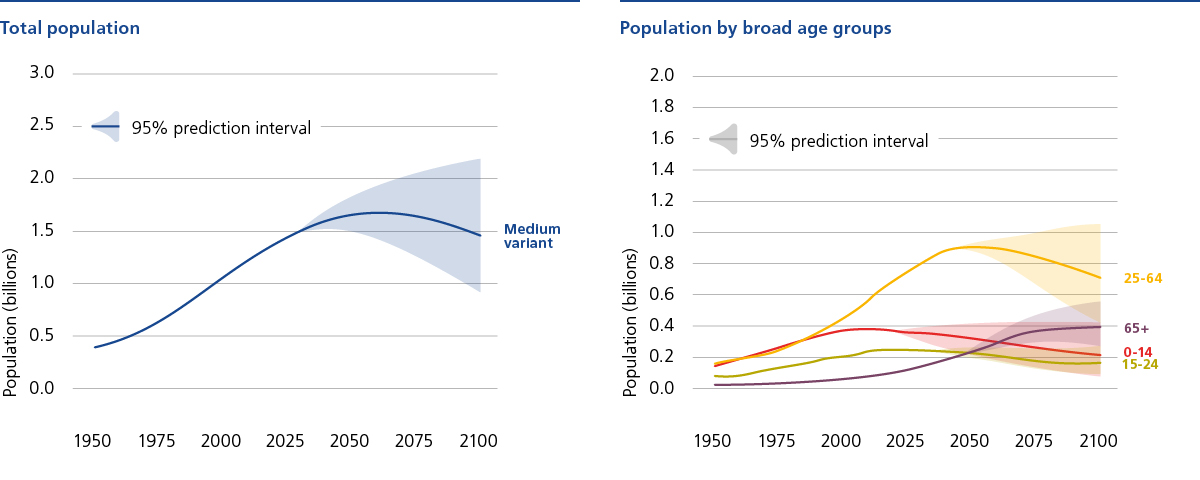

Many years ago China recognised that it would be hard to feed its growing population and introduced a one child policy. This successfully slowed the birth rate, but now the problem is an ageing population. The chart below shows the expected trend with those over 65 rising and the population of working age declining for many years to come. Care of the elderly will put an ever-increasing burden on younger people. For the rest of the world, the growth in the working age population has provided a cheap source of labour over the last twenty years. As the working age population plateaus and falls we will need to find other sources of cheap labour or look for increased automation.

The Communist Party of China (CPC) recognised this danger and have gradually eased restrictions on its original population control policies. They recently went so far as to issue a third child policy to try and reverse the declining birth rate. However, the cost of raising children still means that many families chose to have just one child. This was one of the reasons for the change of education policy, which now prevents foreign involvement and making profits from extra-curricular tutoring. Demographic changes are very slow and hard to change, even if more children are born now they will not enter the work force for many years. While the new policies may be welcome, the damage has been done and the change is coming late in the day.

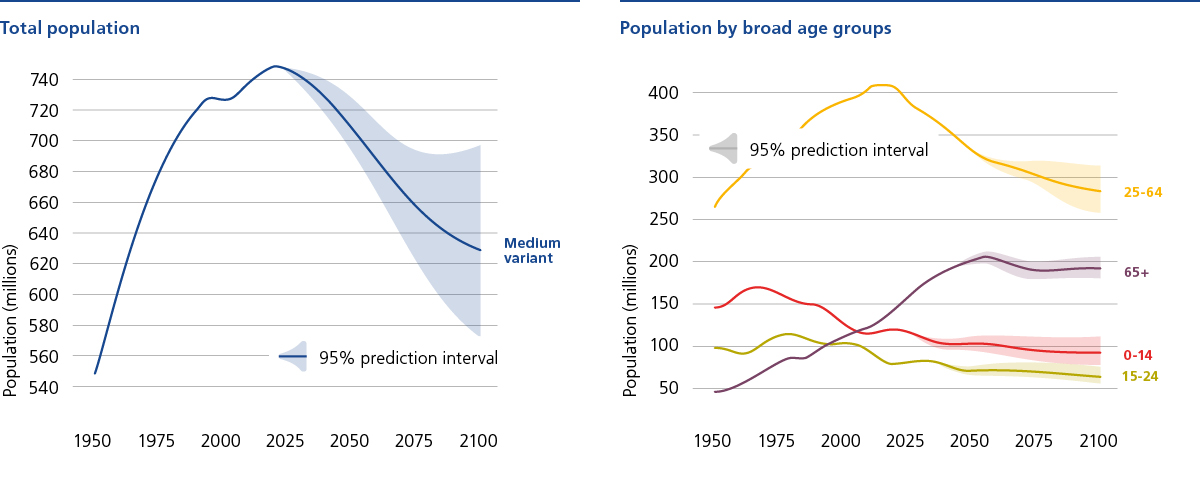

In Europe we have not had a single child policy but the birth rate has also declined. The picture is not as dramatic in Europe as a whole. Migration to many Northern European states has helped offset the falling birth rate.

However, there is a north-south divide. Italy has seen a steep decline in birth rate and many Italians have moved away, seeking work in countries to the north of Europe. In the UK, the decline in working age population and the rise in over 65s means that, unless something changes, there will be close to just one person of working age for each person over 65.

Italy, who already have a large amount of debt outstanding, may find it hard to meet its commitments without the support of its partners in the European Union. Stresses in the Eurozone are likely to continue. If eventually interest rates rise, this will only be made worse.

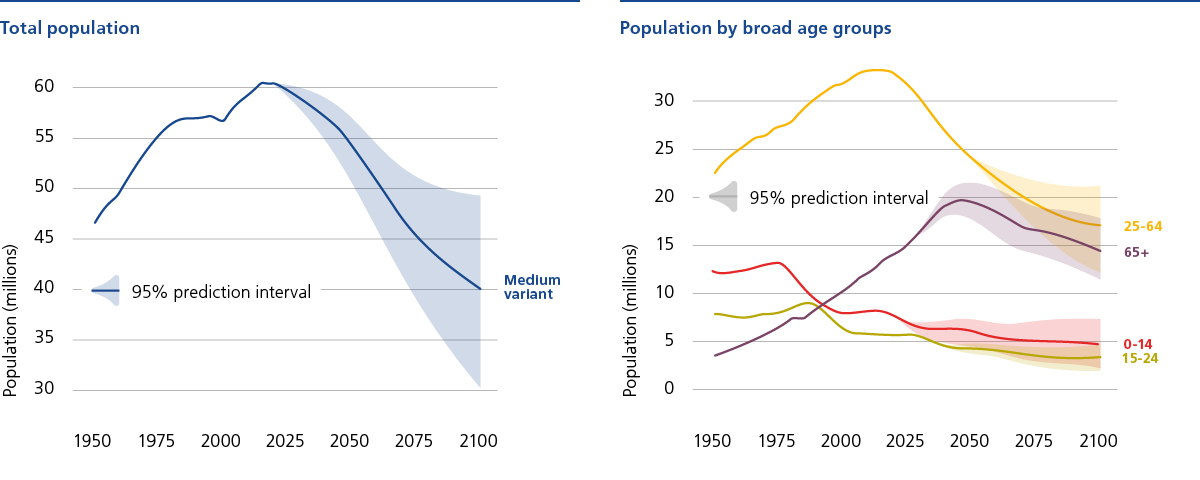

The USA has a similar picture to Northern Europe with less decline in birth rate and immigration offsetting the decline in population. Japan has suffered from an aging population and Japanese companies have moved production offshore.

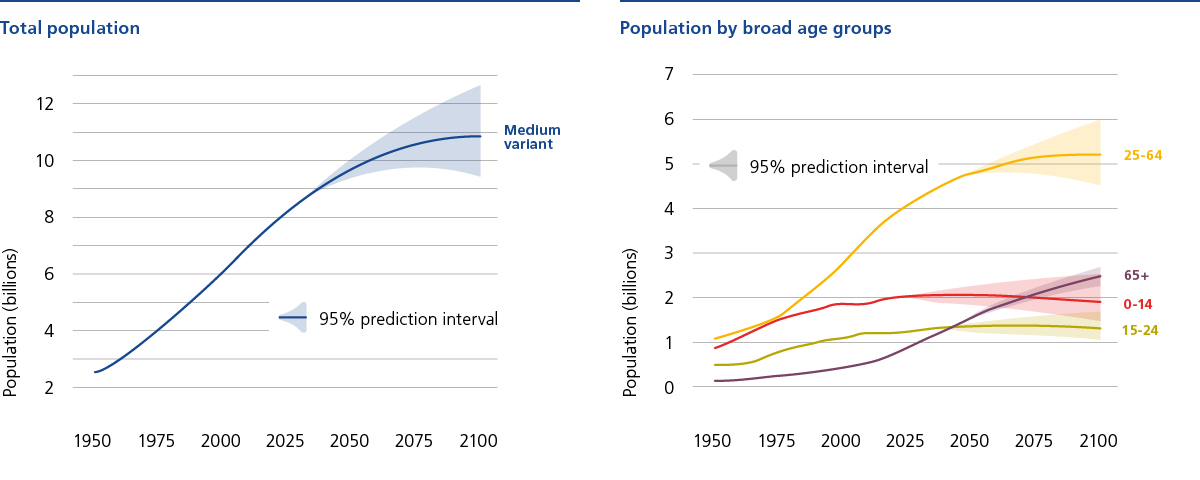

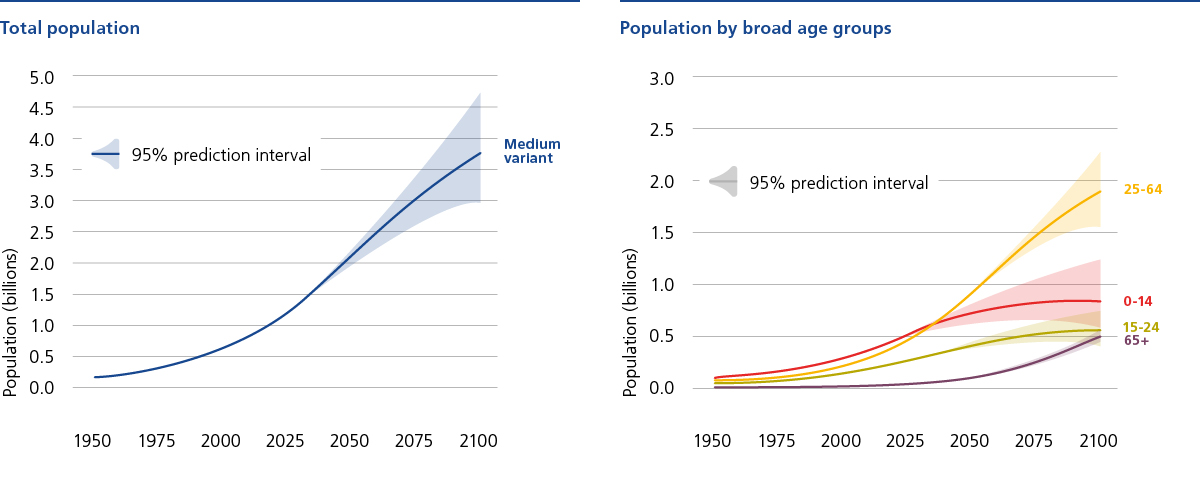

While aging populations are a problem in some countries, as noted above the global population is growing, so where is this growth? The picture is much more positive in some emerging market countries. This is particularly true of India, Indonesia and sub Saharan Africa. If China faulters, then India may be the country best positioned to benefit from a population point of view. However, creaking infrastructure and bureaucracy in India may make this harder and even here after 2050 the trend is expected to reverse.

Sub-Saharan Africa alone accounts for most of the expected growth in the world population. Here the demographics should be clearly positive. However, global warming may hit this region hard. Internal political divisions and corruption make it hard to see this region as source of cheap labour to replace China.

Reading investment implications from trends that are as slow to develop as demographic changes can be dangerous. In general, an aging population is usually expected to be deflationary as the spending power is removed. However, a decline in the working population may see upward wage pressure, which with higher taxes may push up inflation. Deeply indebted nations with increased issuance may have to pay more on their debt. However, debt mutualisation within the EU, if it is expanded, may help spreads on peripheral bonds to remain tight.

Key to getting through this will be technological advancements, including the use of artificial intelligence and robotics. This may require significant capital investment, and the already large tech companies may be best placed to make such investments. Investment in education may be a key factor in achieving the advances needed. The decline in demand, relative to supply, may mean the ever upward move in residential property prices comes to an end. While the demographics in the UK are not as daunting as elsewhere, property price adjustment may become evident in the UK as the baby boom generation hits retirement and looks to downsize. Retirees may sell investments in order to fund their retirement, but this may be countered by those in work saving more as they realise the state may not provide the level of support they will need in retirement.

Unless technology can fill the gaps, adjusting to these changes may be a painful process. Delayed retirement, lower state pensions and higher taxes are all potential solutions, but not likely to be popular vote winners. A set retirement age seems to be a 20th century invention. Up until that time, you worked for as long as you physically could. However, as an Investment Manager, I may work past my state retirement age but don’t think I want to emulate Warren Buffett, who is still investing aged 90.

Demographic shifts are slow and, like a super tanker, difficult to change direction. The worst changes may take some years to be felt. Trends in different parts of the world are radically different and the implications hard to deal with. This year, inflation is likely to rise as we recover from the pandemic and then we expect it to slow again after that. In the really long-term, inflationary pressure may grow again. Moves in markets in the near term are unlikely to be determined by these shifts but we need to be aware of the potential disruption when making longer-term investment plans.