在此处更改您的语言和 LGT 位置。

私人客戶的數碼平台

登錄 LGT SmartBanking

金融中介機構的數碼平台

登錄 LGT SmartBanking Pro

解答常見問題 (FAQ)

LGT SmartBanking 幫助

解答常見問題 (FAQ)

LGT SmartBanking Pro 幫助

Its recent weakness has led to some scepticism as to whether the U.S. Dollar will maintain the position as preferred reserve currency. We provide the basics and weigh the outlook on the dollar's possible role in the future.

A common definition of reserve currencies is that they are foreign currencies held by central banks for investments, transactions, and international debt obligations, among other purposes. A large percentage of commodities, such as gold and oil, are priced in reserve currencies, causing other countries to hold this currency to pay for these goods. As such, these currency reserves can facilitate international trade by minimizing exchange rate risks.

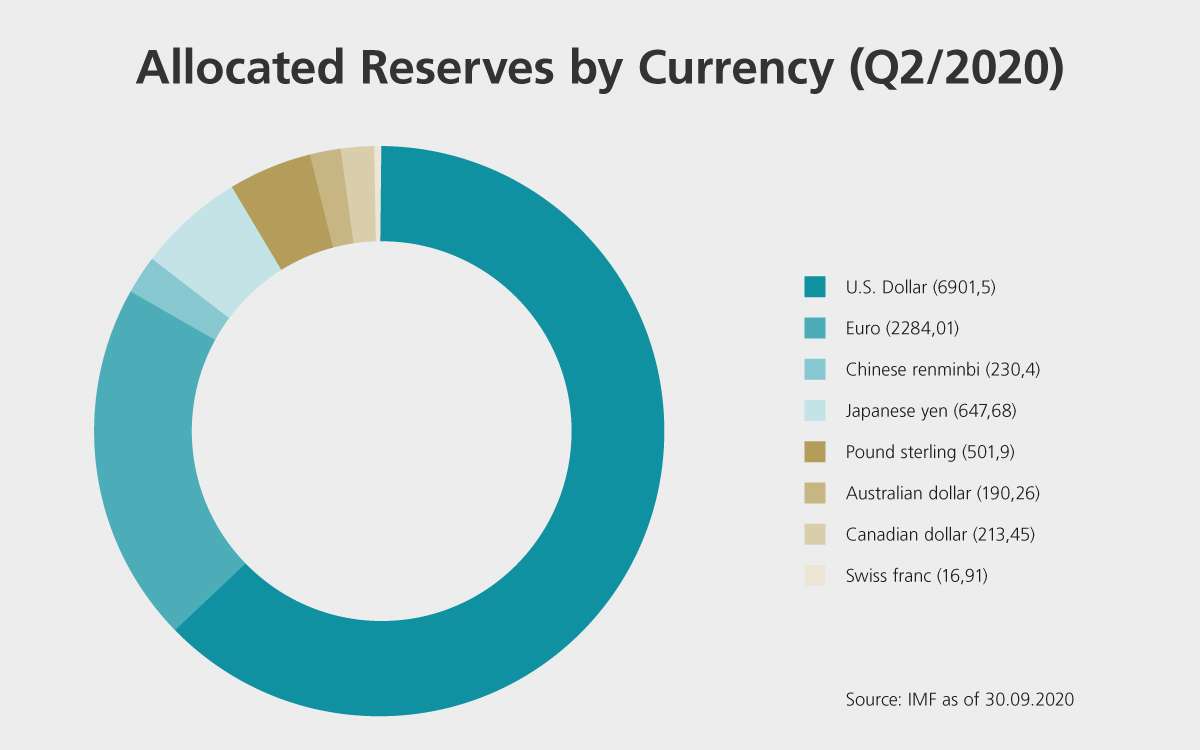

According to the International Monetary Fund (IMF), the currency most commonly held as a foreign exchange reserve is the USD, comprising of nearly 62% of total global reserves as of 1Q2020*. Other major currencies held in reserve include the euro, Japanese yen, and British Pound, which accounted for 20.05%, 5.7%, 4.43% of global reserves, respectively. Although the USD is still the most widely held reserve currency worldwide, it has experienced an increase in competition from the EUR since its introduction about twenty years ago.

While the reserve status is simply a reflection of global central banks' demand for the currency, a reserve currency is usually issued by countries with large economies that have relatively free capital flows and a robust banking system. These requirements have made it difficult for many developing countries to gain reserve currency status and as such, the currencies of China (despite being the world's 2nd largest economy), Brazil, Russia, and India, often referred to as the BRIC countries, are not considered reserve.

As other countries want to hold currency in reserve and use it for transactions, the demand of reserve currencies should be higher, which may in turn lower their borrowing costs through depressed bond yields as most reserves held in the form of government bonds.

After hitting a 3-year high on 20th March 2020, the Dollar Index - a measure of the USD's strength against a basket of six other currencies - has one of its most dramatic slides in years. A key reason why the greenback has been losing momentum can, in our view, be explained by the Fed's expansionary monetary and the massive Covid-19 relief program, which made investors and market participants question the stability of the USD, which is crucial for a reserve currency.

Are you looking for a clearly laid out almanac of the financial world? Do terms like ESG and asset allocation sound greek to you? The financial world is complex - with MAG/NET you get an idea of the big picture.

Learn more in Insights category Financial Knowledge.

While China has experienced rapid growth in the past decades and has become the world's 2nd largest economy, the chance for it to be included as a major reserve currency remains limited, for now. The depth and liquidity of the Chinese government bond market remain limited when compared to those in other major economies, and reserve currencies tend to be held as government bonds rather than hard currency. These limitations, among other factors, makes it hard for the Renminbi (CNY) to obtain a reserve currency status in the near term. Having said that, some experts believe that should economic and financial structural reforms continue, the CNY could become a reserve currency in the near future given its significant share in the global economy.

In our view, we believe the USD will continue to be the most popular reserve currency and it is still the most stable and liquid form of exchange. However, the world would slowly drift away from the USD, and indeed, China, and other emerging powers such as Russia, have been quietly making agreements to move away from the USD in international trade over the past few years. This may lower the demand for the USD and weaken its dominant status as a reserve currency.